Commercial Patterns in Livable Places

A Focus on Commercial Real Estate Development Patterns within the Atlanta Regional Commission's Livable Centers Initiative Study Areas

The Atlanta Regional Commission created the Livable Centers Initiative in 2000, meaning that this year is the 25th anniversary of the initiative. Since 2000, the program has reportedly invested over $312 million in more than 130 communities throughout the Atlanta region, which have gone towards planning studies and the construction of transportation projects.

There’s a large component of the LCI program which is focused on transportation infrastructure and making critical interventions to make places around the region more safe from cars, more walkable and better connected to the region overall through modes of transportation alternative to the automobile. These efforts are highly admirable, however it is not within my skillset to assess the effectiveness of the LCI program in this way. Anecdotally, when I was in planning school we had an assignment where we were asked to analyze a planning document and interview stakeholders about that plan; our plan was the Memorial Drive LCI, which has had the positive impact of persuading GDOT to institute a road diet along the Memorial Drive Corridor in recent years.

Since I am not a transportation planner, my main interest in assessing the impact of the LCI program is in the way that it has or has not changed the composition of the real estate inventories within LCI study areas. While all of these areas have been studied and given attention to this type of human scale, sustainable mode of development at different points during the last twenty-five years, it seemed like an interesting and potentially worthwhile exercise to see how these areas identified by the LCI program have changed since 2000, both as a collective and as individual LCI areas.

Key Takeaways

Multifamily inventory within LCI study areas has increased significantly since 2000, adding 190,441 multifamily units since that time accounting for 44% of the units added in the region over the past twenty-five years. Multifamily development activity, while increased across most LCI study areas, was most pronounced in Downtown, Midtown and Buckhead, which collectively account for 20.8% of regional multifamily growth.

The most significant retail growth among LCI study areas over the last twenty-five years has occurred largely outside of Atlanta across the northern suburbs of the city with pockets of growth to the east and southeast. The growth of retail inventory in LCI study areas has accounted for roughly 33% of regional growth in retail space since 2000, or an estimated 52.5 million square feet. LCI study areas represent some of the best opportunities in the region for walkable, human-scale retail offerings and while not all of the retail in these areas fits that description, suburban-style autocentric offerings unquestionably dominate outside of these livable nodes, meaning retail with a sense of place is still a rarity in the Atlanta region.

Office products remain highly concentrated within only a few LCI study areas, which are located in Intown Atlanta, Perimeter and North Fulton, which collectively account for roughly 39% of the region’s office production since 2000, with all LCIs together accounting for an estimated 58% of this growth. While office space remains concentrated overall, there are far more pockets containing small amounts of office space within suburban LCI study areas than there were prior to 2000. Addiionally, while office space remains concentrated, in-office modes of work are no longer the only format available to workers, with hybrid and remote options allowing suburban residents to play a more active role in the daytime retail ecosystems and communities of suburban LCI study areas.

About the Data & Areas for Future Exploration

The data included in this post comes from CoStar property exports that were analyzed using ArcGIS Pro and Excel; unfortunately, CoStar’s user interface makes it very time consuming to export market data for each LCI study area, as it does not allow users to upload Shapefiles, meaning that custom areas would have to be drawn for each one in order to extract market profiles.

Because of this, I can’t speak to how the vacancies and rents for real estate products in LCI study areas have performed over the last twenty-five years, but I can report on the way that these study areas have captured new deliveries since 2000.

An additional layer of analysis that I hope to perform in the future is to take a look at the commuting inflow and outflow of each of the study areas to try to better understand which study areas have become the most “livable” in terms of increased retention of residents as part of the area workforce. Census data may also provide an interesting if inexact examination of demographic transition within each study area.

Pan-LCI Shifts in Commercial Real Estate

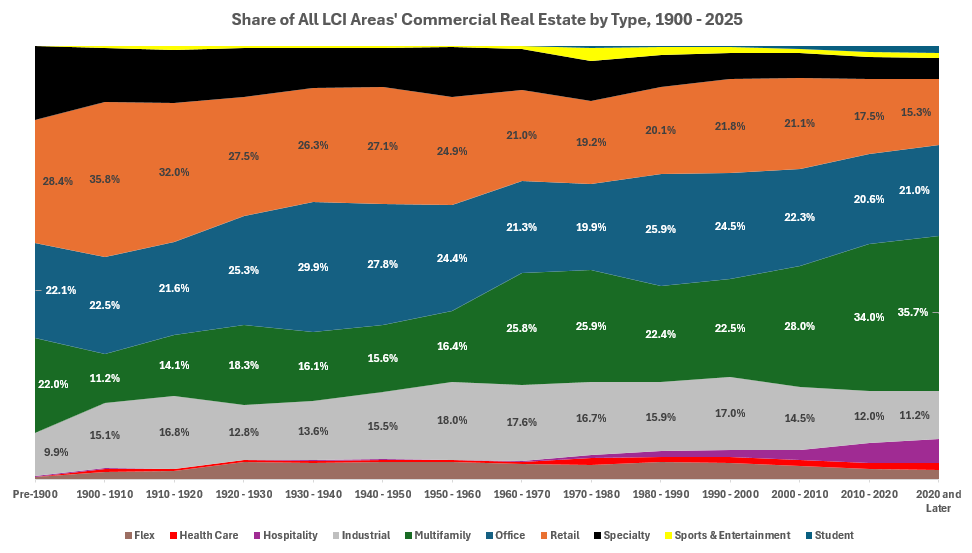

Regardless of whether a given LCI was studied in 2000 or in 2024, these areas represent the places within the Atlanta region where opportunities for walkability and transit-oriented development are the greatest. Many LCI study areas represent existing town centers, others are busy commercial corridors, still others are commercial districts anchored by dead or dying malls and some are office districts that historically became ghost towns after workers had gone home. Many of these study areas were significant areas within the context of the Atlanta region far before they were every LCIs. The graph below shows how the distribution of commercial real estate has changed over time within these areas that have been designated as LCIs since 2000.

There is not a true science to determining the best mix of real estate property classes to make a place feel alive; places that have a high amount of retail but not as much multifamily may still feel vibrant because they serve as centers of wider communities, places with a high number of multifamily units may still feel quiet and residential because of limited retail and office options within walking distance. For this reason, an attempt to assign a “grade” to each of the LCI study areas in terms of their mix and how that has changed over time was abandoned because success and vibrancy can take many different forms. What we do generally know is that vibrancy does require a mix of uses, and many of the region’s LCI study areas have diversified their commercial inventory greatly since 2000.

Multifamily

44% of regional multifamily units delivered

190,441 multifamily units

Much of this gowth was concentrated in Midtown Atlanta and Buckhead.

Other significant growth areas were Downtown Atlanta, the Memorial Drive Corridor, the Upper Westside, Perimeter, Cumberland and Gwinnett Place.

Retail

33% of regional retail square feet delivered

52,456,025 square feet of retail

Many of the LCI study areas with the highest amount of retail growth since 2000 were located in the northern suburbs of Atlanta, with areas such as Gwinnett Place, Sugarloaf, North Point and Milton capturing the highest share of regional retail growth.

While retail space created within these LCI study areas is not guaranteed to be the walkable, experiential, human-scale products that we’d like to imagine them to be, it is relatively safe to assume that very little retail fitting that description was built outside of these study areas, meaning that suburban style auto-centric retail space has continued to be the dominant form of retail delivered in the region since 2000.

Office

58% of regional office square feet delivered

93,150,124 square feet of office

While collectively LCI study areas accounted for over half of the growth of office space in the Atlanta region since 2000, this growth remains highly concentrated in Midtown Atlanta, Downtown Atlanta, Buckhead and Perimeter.

Areas that experienced some growth in office space capturing less than 5% of regional growth in office products include the Upper Westside, Beltline Subarea 7, Cumberland, North Point, Milton, Peachtree Corners, Gwinnett Place and Sugarloaf.

Hospitality

66% of regional hotel rooms delivered

51,620 hotel rooms

Much like office, the growth in hospitality products within LCI study areas represented the majority of the growth in this property class since 2000, with most of this growth occurring within only a handful of LCI study areas, notably Downtown Atlanta, Midtown Atlanta and Buckhead, which have historically possessed the largest inventory of hospitality and office products.

A handful of study areas outside of Atlanta captured a fair amount of regional hospitality growth, with much of this growth mapping on to growth trends in suburban office.

Student Multifamily

71% of regional student multifamily units delivered

9,144 student multifamily units

Student multifamily is a much more niche product type, but can still play a significant role in activating an area. There were very few places within the region that had any student multifamily inventory in 2000 and regional growth in this inventory was highly concentrated within seven study areas: Midtown Atlanta, Upper Westside, Downtown Atlanta, West End, Turner Field (Summerhill), Marietta University District and Town Center Mall.

Final Thoughts on Twenty-Five Years of Livable Centers

The Atlanta Regional Commission’s Livable Centers Initiative represents an important step towards the region’s urban evolution from a nebuloid cloud of residences and auto-centric strip centers arranged around a dense core city into something closer to resembling a solar system in which Atlanta is the bright sun at the center and these livable centers beyond it are the planets that orbit it. The enduring concentration of office space within the core city and the perpetuation of auto-centric retail development suggest that the LCI program alone will not have the power to move the needle on curbing sprawl and auto-centric development patterns broadly, not that we expect that much of the program. While acknowledging that any transition that has occurred across the LCI study areas is not necessarily attributable to the LCI program, it is heartening to see the massive increase in multifamily projects across all of the LCI study areas. Retail follows rooftops, and where there are people there is built-in demand for services and perhaps, in time, opportunity for spatial decentralization of the region’s job cores.

Whether it is true or not, there have been suggestions that ARC intends not to create any new study areas moving forward, with their future work on LCIs aimed at solving more complex problems related to the feasibility and financing of creating more walkable, mixed-use nodes across the region. If this is the case, my sense is that pushing for greater connectivity between these nodes in ways that do not require a car will be an important key to unlocking new potential.

People want to be able to leave their house and walk to the coffee shop on the corner on Saturday mornings, but residents of the Atlanta region are also metropolitan; they are interested in enjoying the variety of food, entertainment and specilty offerings that are unique to Atlanta and not necessarily located in their neighborhood. The only way that Atlanta residents, even those living in the region’s livable centers today, can enjoy all that Atlanta has to offer is by owning a car, which means parking can never be abolished, which means we need parking decks or surface parking, which means less new multifamily units, less retail space, less office and that it all is more difficult for developers to finance and less accessible to households and businesses.

The Atlanta region lacks a strong centralized entity that is able to exert planning powers throughout the region, it is not definitive whether the region should have such an entity or not. While the Atlanta Regional Commission is the closest thing that we have to that, it cannot compel cities and counties to prioritize more efficient and more sustainable development patterns. My hope for the future of the LCI program and for the ARC in general is greater influence over local planning and greater capacity to assume the risk that is involved in helping our region evolve from a sprawling, placeless one, to an interconnected web of interesting, human-scale places.

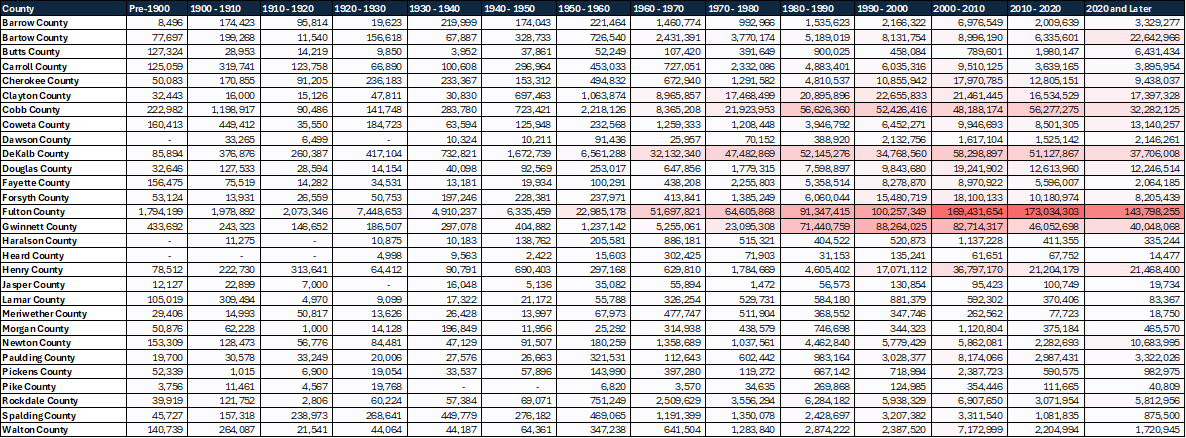

Real Estate Development Trends in the Atlanta Region: 1900-Present

In the process of examining the changes in ARC’s LCI study areas since 2000, I ended up having to download far more data than I needed, presenting me with an extra opportunity to take a look at patterns in commercial real estate development in the region back to 1900.

Additionally, I am always interested in where new development activity is taking place within the Atlanta region and how that compares to historical trends. In my work and in conversations with other planning-minded friends and colleagues, the narrative that I am often trying to advance is that “place” is becoming a necessary element for successful real estate development, but it’s always important to check whether that actually holds up.

Key Takeaways:

Development prior to World War II was largely concentrated in Atlanta with smaller hot spots in other historic downtowns around the region.

Post-War development didn’t really take off until around 1970, at which point development activity boomed north of Atlanta through the 1990s.

Development throughout the 2000s largely matched the spatial trends of the 1970s through the 1990s, however deliveries occurred in much smaller volumes.

The 2010s, which we recognize as the decade following the 2008 financial crisis and also the decade of gentrification and the “return to the city” saw much more activity again concentrated within the heart of the region in Atlanta.

Since 2020, development activity has stretched out even further than before largely following the I-75 corridor both north and south of the city and the Highway 400 corridor north to Dahlonega.

Data Sources for all maps and charts come from CoStar and from the Atlanta Regional Commission’s Open Data Portal.